Keywords

How to Cite

Abstract

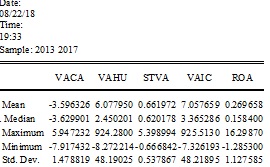

Background : The phenomenon of Intellectual Capital (IC) began to develop in Indonesia, especially after the emergence of PSAK No. 19 (revised 2000) on intangible assets. According to PSAK No. 19, intangible assets are non-monetary assets that can be identified and do not have a physical form and are held for use in producing or delivering goods or services, rented out to other parties. Method : The data used in this study is Data Cross Section (Panel Data) from 79 financial sector companies in Indonesia from 2013 to 2017 which are listed on the Indonesia Stock Exchange (IDX). The method used: Panel data multiple regression with Eviews 9 software is used as a tool for selecting a regression model to test the Effect of Intellectual Capital on ROA. Result : The results of this study indicate that: the variables VACA, VAHU, STVA and VAICTM have a significant effect on ROA, with the findings of the four variables of Intellectual Capital used, the most dominant variable affecting ROA is Value added human capital (VAHU). Conclusion : Value added capital employed (VACA), Value added human capital (VAHU) , and Structural capital value added (STVA) have a significant effect on Return on Assets (ROA or Value added intellectual coefficient (VAIC™) has a significant effect on Return on Assets (ROA).

This work is licensed under a Creative Commons Attribution 4.0 International License.

Copyright (c) 2023 Lembaga Layanan Pendidikan Tinggi Wilayah X