Keywords

Time Budget Pressure

Competence

Audit Experience and understanding of information systems

How to Cite

Abstract

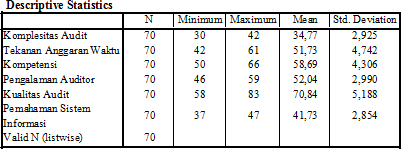

The purpose of this research is to examine the effect of audit complexity, time budget pressure, competence, and auditor experience on auditor quality with an understanding of information systems as a moderating variable. The population is taken from auditors at KAP in Medan, where the total population is 100 auditors. The sample was taken using the purposive sampling method with the criteria (1) having an education of at least a Diploma (2) having a work experience of at least one year, because they already have experience and time in carrying out adaptation and providing an assessment of their performance and working environment conditions, therefore the sample is 70 respondents. Here the data are analyzed using multiple regression and moderation assisted by the SPSS 20 program. The results of the hypothesis tested in this study show that the competence and experience variables of auditors have a negative influence on audit quality, but through the interaction of the moderating variable understanding of information systems, the competence variable brings changes. the direction is positive, but in contrast to the auditor's experience through the interaction of the moderating variable understanding of information systems, the auditor's experience variable does not change direction. Meanwhile, the time budget pressure variable and audit complexity positively affect audit quality even with the existing interaction of the moderating variable understanding of information systems, the audit complexity variable still affects audit quality positively, but differs from the time budget pressure through the interaction of the moderating variable understanding the information system pressure variable. time budget changes direction to negative..

This work is licensed under a Creative Commons Attribution 4.0 International License.

Copyright (c) 2023 Lembaga Layanan Pendidikan Tinggi Wilayah X